In case you are interested in the composition of my work on evidence-based policy advice regarding Ecological Fiscal Transfers, here is my dissertation (submitted in December).

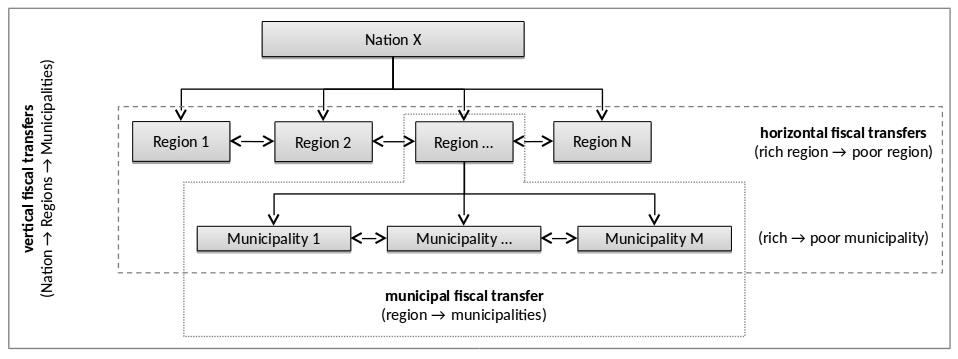

Below, you find kind of a graphical abstract. Take it with an imaginary teaser: suppose that some portion of fiscal transfers is dedicated to the existence of protected areas.

Overview of fiscal transfers in multilevel governments. Source: Droste et al. (2017), p. 332.

Does that increase the designation of protected areas? Check out my dissertation.

Let me know if you have any questions, requests, or offers ;).

letting the data speak: Latent Dirichlet Allocation

We have analyzed topics in ecosystem service research through a fancy unsupervised machine learning algorithm developed by Blei et al. (2003), called Latent Dirichlet Allocation, which we use to analyze how the content has developed and changed over three time periods from 1990 to 2016.

The interactive plots for the subset periods can be found here:

I am back from a fabulous experience in Peyresq, France, at the ALTER-Net Summer School. It was an intense 10 day summerschool on biodiversity, ecosystem services, and science-policy interfaces in a gorgeous village in Alpes-de-Haute-Provence.

Five elements contributed essentially to the extraordinariness of the experience:

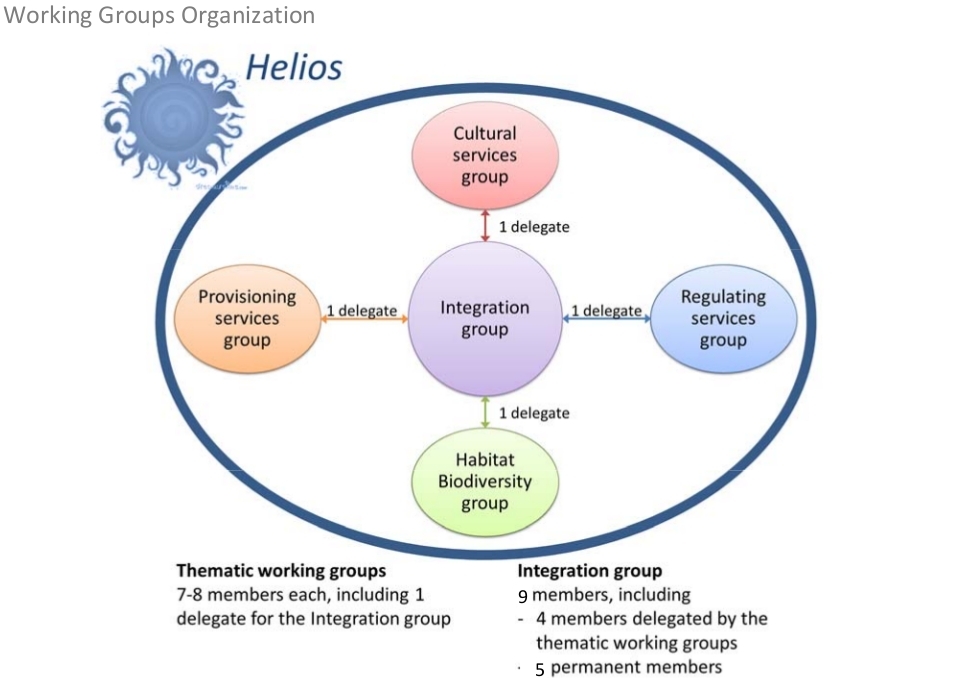

We were working on a project: “How to maintain wellbeing and biodiversity in the upper Verdon Valley?” (Helios). Within 7 days we were to deliver an analysis of the current status quo including trends, develop scenarios, assess trade-offs and synergies, propose policy-measures and present the findings. A challenging task which - after we had settled for understanding it as a simulation without the need to do all these steps in all possible detail - became great fun! The original working group proposal looked like this:

Source: ALTER‐Net Summer School 2017

Working group project preparation document

In the end, we had developed a far more complicated, yet effective structure with further special taskforce groups on trade-offs and synergies, policy proposals, creative communication, and the scenario envisioning. We were delving into a lively and really inspiring collaborative process, that has taught me a lot on structures and collaboration.

A really helpful lesson was the technique that was employed: Kanban, which allowed to transparently and flexibly schedule, prioritize, breakdown, implement and validate tasks within working groups. It is really worth being tried! It even inspired a couple of songs that were composed in our leisure time.

Peers

Getting in touch with 34 highly skilled young scientists from not just Europe but all over the place was a great source of inspiration. Very bright minds! I am quite sure a couple of us will remain connected and strive together towards solving the world’s socio-ecological crises! I am deeply grateful for you partaking in this experience. Imagine all us people, working for the world (sorry, this is an insider)!

Peyresq

Source: Ph. Malburet

A beautiful, refurbished historical mountain village, remote, without high-speed internet, named after the French humanist Nicolas-Claude Fabri de Peiresc and one of the best places I have been so far. The staff was very friendly and the food was delicious. Perfect for hosting the summer school!

For me this was a 100 per cent recommendable experience. If you ever have the chance to attend – do it!

Bartosz Barkowski and I, we wrote a reply to Obst, Eden and Hein’s article on ecosystem services valuation for national accounts. I have also published a blogpost at the German Ecosystem Service Partnership website here – which is in German, though. At this site I will only give a brief summary of our main points – whoever is interested is welcome to request a version of the reply in case it cannot easily be accessed.

In my view, one of the main lines of Obst et al.’s article is that the valuation methods for ES accounting need to be consistent with the standards for national accounting in general. That is just fair enough – any inconsistency would not allow for a proper comparison of the industrial economic output and the ecological effects of production. The very essence and main purpose of ecosystem would be counteracted. ‘

Given that there needs to be a consistency, there still remain questions about Obst et al.’s conclusions regarding certain valuation techniques. Here is a summary of what we think has not sufficiently been considered in their argument.’

(1)

They say: Accounting (gold) standard is to use market prices – irrespective of market conditions and failures (!). If no market value is available proxies for market prices have to be used. A range of estimation methods are available but shadow prices are not okay since they are not consistent surrogates for market prices for being used in welfare accounting instead of national accounting.

We say: Right. Market prices are standard. Proxies need to be used when no market prices is available. Welfare accounting uses shadow prices and they are not necessarily equal to market prices. Shadow prices are supposed to be the “true” value a good or service marginal contribution to welfare. They do not include market failures. But for public ecosystem services where there is no market, we cannot assume that a hypothetical market price for and the shadow price are different unless we also assume a hypothetical market failure.

Who would want to estimate a hypothetical but already distorted price for an ecosystem service for national accounts? Isn’t it better to try to estimate the value of an ES for accounting purposes as close to their “true” value as possible?

(2)

They say: Stated preference methods are being used for welfare accounting such as cost-benefit analysis and consumer rent analyses (which is basically the area under the demand curve down to the price level, whereas producer rents are the area above the supply curve up to the price level – and both are supposed to be a measure of the resulting net benefits of market transactions for the respective group). Therefore they cannot be used for accounting since accounting requires to estimate value by price times quantity – which is the area up to the price level and up to the traded quantity.

We say: Right. Stated preference methods have been used to estimate consumer rents and the like. But they can also be used to estimate a marginal price at a given quantity. Therefore, we cannot exclude them from accounting usage only because they are also used for other methods. Furthermore, if we do not know how much people want (and stated preference methods estimate a willingness to pay as a surrogate) a certain ES, how do we know whether production level of that service are below (or above?) the socially desired levels?

How can we refrain from cross-triangulating accounting values with different sources of information if we want them to be as exact as possible? Aren’t people’s preferences are one of the central sources of information on goods and services not traded in any market?

(3)

They say: Values of non-marketed assets are to be accounted for via net present values (a discounted sum of all future flows). Depreciation for these assets is valued at written-down replacement costs (what you would get for the asset in a hypothetical market, which basicallyis initial price minus depreciation times years of usage). Restoration costs are not a accounting equivalent to depreciation – because depreciation measures a change (decline) in future flows. Restoration costs are what it would cost to restore / replace the asset in a condition without the loss of value. Hence, the loss in ecosystem services stocks cannot be evaluated with restoration costs but should be valued at replacement costs.

We say: Capital stock values may decline over times, e.g. through usage and a declining remaining life-time. Ecosystem asset values may decline through non-sustainable use (because productive capacities only decline through over-usage). Depreciation measures a loss in value from one period to the other. Restoration measures the loss in value from one period to the other. Both account for a change in value from one period and can thus be considered equivalent.

How can we value degradation with replacement costs if that implicitely assumes a substitutability? Isn’t sustainable development about maintaining the possibilities for future generations? How can we surely know that an ecological asset can be replaced by man-made alternatives?