21 Aug 2022

About four years into my assistant professorial position, I have recently been granted a venia docendi in the house of knowledge ;)

Academic hat and diploma, from public domain vectors.

I am now Docent in Environmental Politics at the Political Science Department and Environmental Politics Research Group; deputy theme leader in the biodiversity theme Biodiversity and Ecosystems in a Changing Climate. And, I am fellow at the Centre for Innovation Research.

Most importantly, this means I am now formally allowed to supervise PhD students as a main supervisor.

Got a couple of research projects going on: GreenPole and Mistra Biopath are possibly the biggest of them.

For more detail check out my CV

01 Dec 2020

About a year into my new position, I have now dived into teaching. Immersed really.

I like it a lot - especially when students are happy about the course design and its didactics.

Recently, I have taught, together with Fariborz Zelli, now for the second time, the ClimBEco course on

Global Environmental Governance Today – Actors, Institutions, Complexity

We apply a mixture of theory heavy lectures and much more applied seminars and simulations, and even had a game of Bruno Latour’s Politics of Nature as a premier this year. The concept has just won the Prize for International Student Teaching by the ECPR Standing Group Teaching and Learning Politics. Lucky us, the students seemed to like it, too ;D

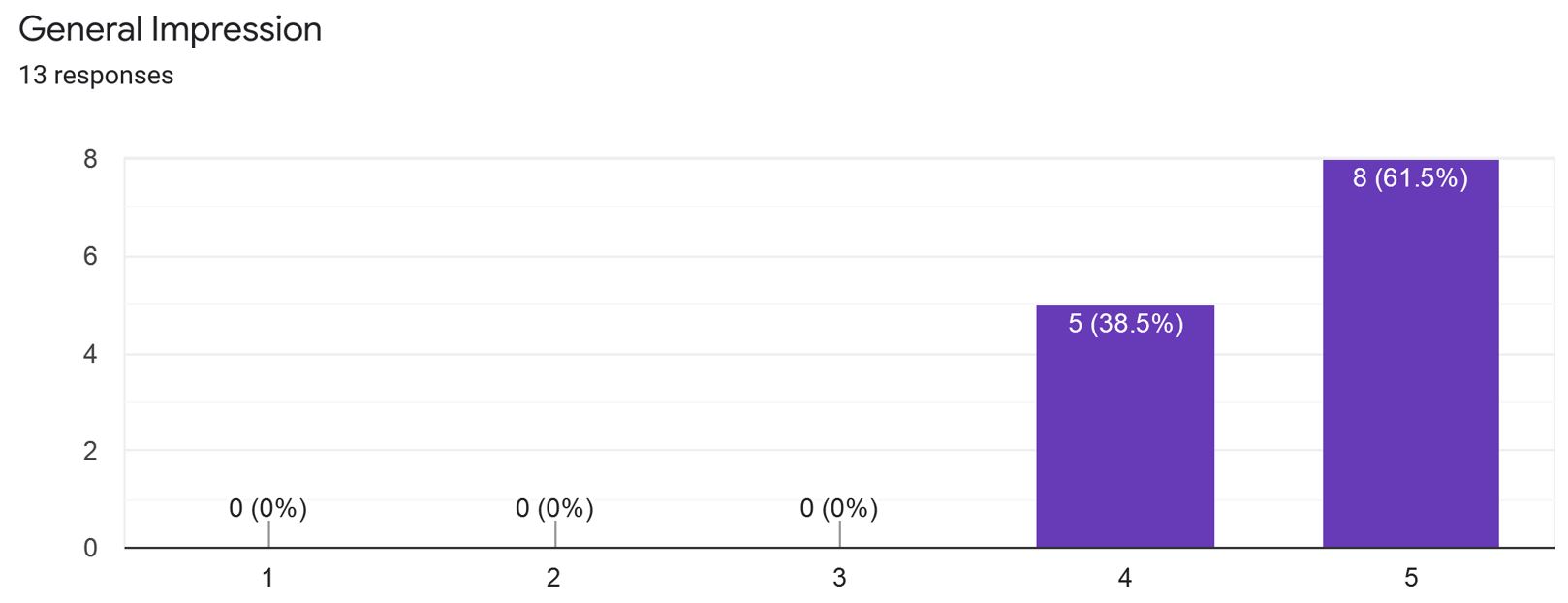

Student responses on a scale from 1 (super useless) to 5 (super helpful), 50 % anonymous response rate.

01 Sep 2019

Social Science Faculty building, own pic.

In September I have started as Associate Senior Lecturer (Biträdande Lektor) in Environmental Politics at the Political Science Department in Lund. My position is co-financed by the strategic research area Biodiversity and Ecosystems in a Changing Climate. I will also form part of the Environmental Politics Research Group. Method wise, I will be one of the few scholars bridging social and environmental science through quantitative methods. Teaching wise, I will be part of the teams for “International Environmental Governance” and “Methods in Social Science”. This four year, tenure-track position is going to a super exiting interdisciplinary and hopefully trandisciplinary journey!

I really want to get my hands dirty with some applied and evidence-based policy advice for effective conservation policies ;)

10 Aug 2019

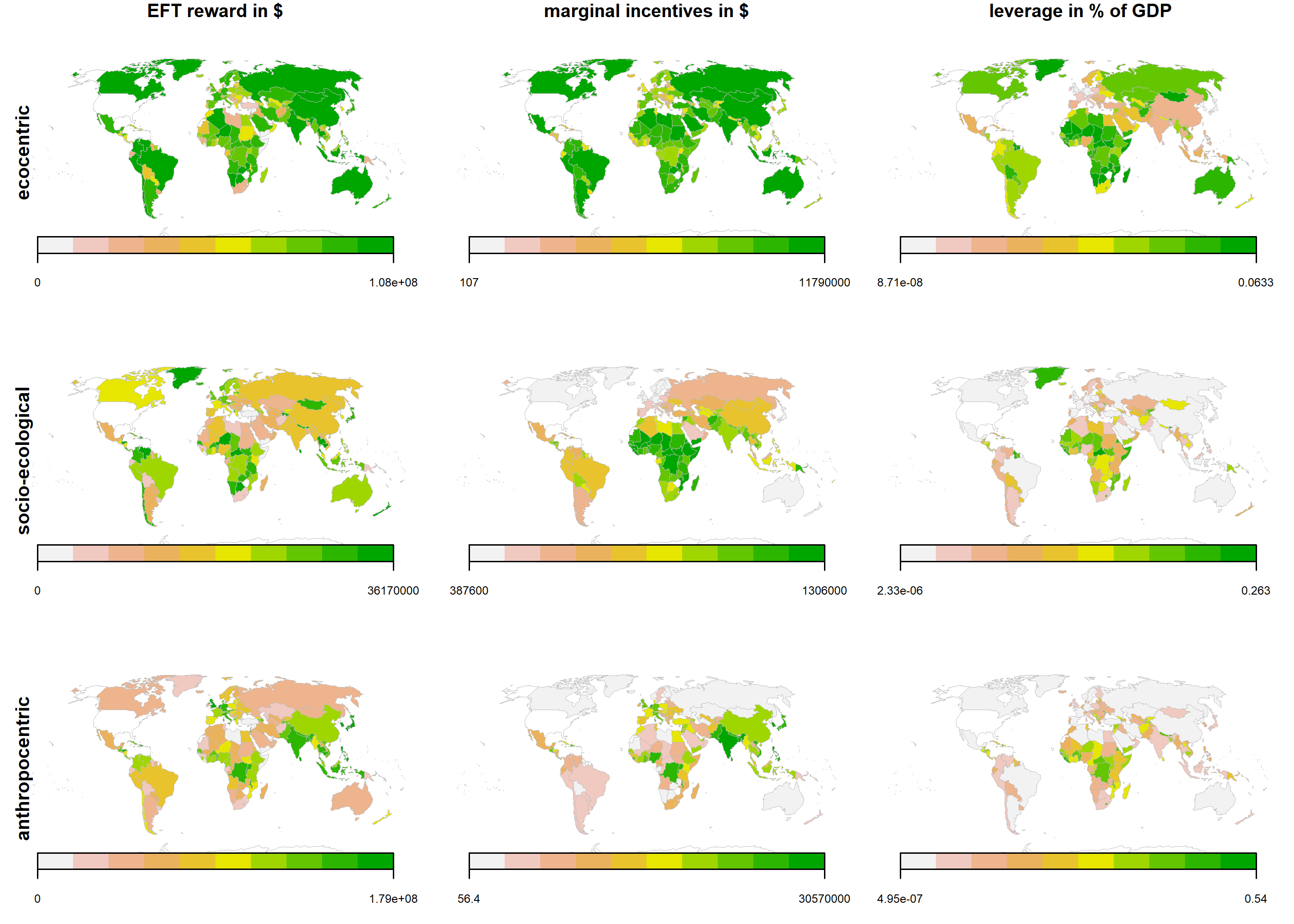

Global distributions of rewards, incentives, and their leverage, doi: 10.1111/conl.12670

In a recent article Georgina Mace et al. propose to aim higher to bend the curve of biodiversity loss. While I am convinced that this is not just needed for sustainable development but also feasible, I do think we need to innovate our (global) institutions to make such a change happen.

With the current IPCC Land report and the global IPBES assessment, it is clear that land use has to change. Nature Conservation and protected areas are cornerstone in any strategy to safeguard ecological life support and thus human thriving.

So, what if we paid nations for their conservation efforts? Gave them a financial reward for providing protected areas? This is the basic idea of the Brazilian Ecological Fiscal Transfer systems, that compensates municipalities for hosting protected areas. According to the empirical results so far (e.g. here, here, and here) this sets incentives for conservation that result in additional protected areas.

Therefore, we propose to upscale such an EFT mechanism to the global level and developed three different design options:

- Ecocentric: only protected area (PA) extent per country counts, the bigger the protected area the better

- Socio-ecological: protected area and Human Development Index count, to bring in some development justice

- Anthropocentric: population density is also taken into account, because people benefit locally from PA

We assess the designs by how well they perform in setting incentives with regard to policy gaps to reach Aichi target 11. Here, we find that the socio-ecological design sets the highest incentives where the policy gap is largest.

By this we hope to inspire some constructive science-policy dialogue about how we can devise institutions to make land use change happen and bend the curve of biodiversity loss.

The article has been published open access in Conservation Letters:

- Droste, N., Farley, J., Ring, I., May, P.H., Ricketts, T.H. (2019) Designing a global mechanism for intergovernmental biodiversity financing. Conservation Letters. doi: 10.1111/conl.12670

25 Jun 2018

Lund University Library, own pic.

I have just accepted a post-doc position at the Center for Environmental and Climate Research (CEC) in Lund, within the strategic research area Biodiversity and Ecosystem Services in a Changing Climate (BECC). I am going to work with Mark Brady, Katarina Hedlund, Yann Clough, Wilhelm May, Luca Di Corato, and Yves Surry on the insurance value of soil biodiversity with regard to increasing weather variability. The project is called, ”Biodiversity and Ecosystem Services as Insurance against risks of Future Weather Variability (BioInsure)”. I will be starting in September.

I am super excited!